The 10-year Hold Test

What two insurers taught me about change, compounding, and capital allocation

A couple of years ago, I had lunch with another fund manager, and our conversation, as usual, centred on the companies we own. He observed that, while he owned several companies for a decade (or longer), the businesses had changed so much over that period that they were almost unrecognizable. This gave me an idea to take a deeper look at how the two companies I owned for more than a decade, which happened to both be insurance companies, changed over time.

Travelers Co (TRV) is a traditional regulated insurer. It stands out in the market by selling commercial and personal property/casualty insurance through a network of independent agents and brokers. While this approach may seem outdated to consumers accustomed to online comparison sites, as of 2023, it remained the dominant distribution channel for most insurance lines.

Commercial, workers’ compensation, and other lines are an area of strength for Travelers, which is 80%+ reliant on independent agents who sell insurance to small and middle-market businesses. These agents work with the businesses to understand each company’s unique situation and tailor the insurance offering to its needs.

In 2024, Travelers’ segment breakdown looks similar to that in 2013, with more than half of premiums coming from commercial insurance lines. Curiously, one area of outstanding growth has been personal auto insurance, where the company continues to compete effectively despite strong competition from DTC operators such as GEICO and Progressive.

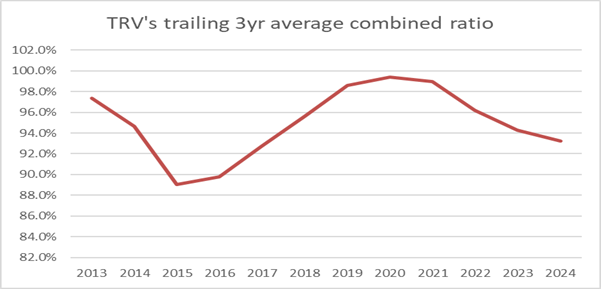

Over the last decade, Traveler’s gross written premiums (GWP) grew by roughly 5% per year, in line with the growth of the overall P&C market. Underlying profitability also remained roughly the same, with the combined ratio, a key measure of insurance company profitability, fluctuating between 90% and 100% for most years.

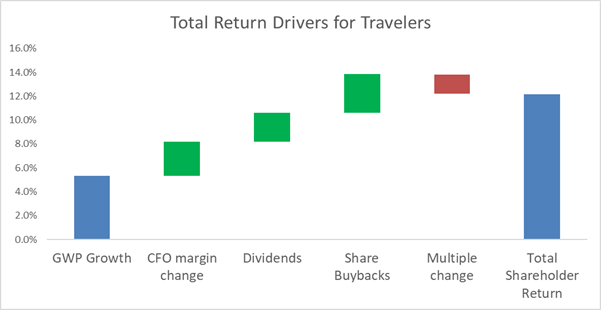

The company’s solid yet admittedly unremarkable performance raises the question of whether it is a good investment and why. The answer, as usual, is in capital allocation. For the companies I am considering I try to understand what the drivers of returns have been and split them into fundamental (revenue growth and margin changes), capital allocation (dividends and buybacks) and market specific (multiple expansion). The reason for this exercise is that I believe returns are more sustainable when they come from fundamental or capital allocation factors while market multiple expansion at some point, in theory, will meet its mathematical constraints.

Over eleven years, Travelers generated $66 billion in operating cash flow, which is roughly equivalent to the company’s current market cap. Roughly half the amount contributed to the investment portfolio, which supports insurance operations and now stands at about $100 billion. At the same time, the other half was returned to shareholders as dividends and buybacks. Since 2012, the average dividend yield has been around 2% and repurchases reduced shares outstanding by over 30%.

Thanks to the smart capital allocation decisions, Travelers turned what would have been a solid 8% p.a. growth in intrinsic value into a 14% annualized increase. Curiously, in the market constantly in search of compounding machines, Travelers, despite its size and solid execution, has been largely overlooked, with a total shareholder return of 12% p.a., which lagged the intrinsic value creation.

The second insurance company, a holding since 2012, is Assurant Inc (AIZ). Assurant, a significantly smaller company with a market cap of around $11 billion compared to Travelers’ $65 billion, has a unique business model. It specializes in two niche insurance types – extended service contracts for consumer electronics and lender-placed home insurance. Despite their apparent differences, both businesses share a common trait: the separation between the decision-maker and the payer, a factor contributing to Assurant’s healthy profitability.

For extended service contracts, rates are negotiated with mobile service providers and paid by customers who choose to add this feature to their mobile plans. Mobile operators are encouraged to upsell this service through commissions and profit share arrangements.

Lenders force lender-placed home insurance on homeowners who need to obtain adequate coverage on their own. Lenders care only about the quality of the insurance provider, not about the cost of the insurance passed on to homeowners. Selling a product to a buyer who cares more about quality than price generally results in healthy profitability for the provider. Assurant’s lender-placed home insurance is no exception, with the margins from this business usually hovering around 10% — a very healthy level for an insurance company.

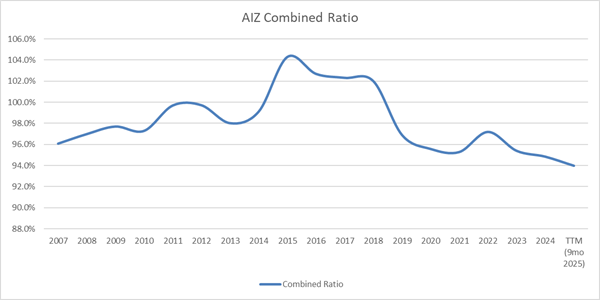

While Travelers Co. looks largely the same as it did ten years ago, the same cannot be said for Assurant Inc. (AIZ). Ten years ago, extended service contracts and lender-placed home insurance accounted for roughly 60% of premiums, with the remainder made up of health insurance, employee benefits, and pre-need funeral expense coverage. These other lines were sold off in a series of transactions for a total of around $2.3 billion. In exchange, Assurant purchased The Warranty Group for $2.5 billion in cash and shares. The acquired company had a significant presence in extended service contracts and automotive extended services coverage.

These transactions, which took place between 2016 and 2021, reshaped Assurant Inc. While revenues from premiums remain roughly the same, the company is now more concentrated in segments where it has clear competitive advantages and a healthier level of profitability. The combined expense ratio has improved, dropping from roughly 100% of premiums to around 95%, indicating a more efficient operation.

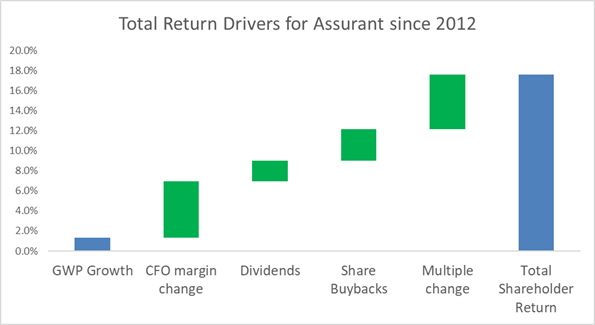

Regarding the shareholder return drivers which I’ve illustrated in the chart below, margin expansion and shareholder returns have been the primary source of value creation over the last decade. Growth in premiums is relatively pedestrian at 2%, but the M&A transactions obscure it. The core segments of extended warranty and global housing have grown steadily, averaging 4% per year since the acquisition of The Warranty Group. Capital allocation is once again value-accretive, with an average dividend yield of 2% and annualized share buybacks of around 3% since 2012.

Unlike with Travelers, shareholders of Assurant benefited from multiple expansion. Given improvements in the underlying business quality it is arguably warranted in this case. Even with multiple expansions, the AIZ is not particularly expensive,

trading at a P/E of 11 and almost 10% FCF Yield.

The examples of Assurant and Travelers show that while good managements and companies may take different paths towards long-term value creation, truly exceptional results are unlikely without superior capital allocation, which can take the form of accretive M&A or appropriately sized buybacks conducted when the market offers the ability to buy high-quality businesses at high free cash flow yields.1

Takeaways:

- Very few companies look the same as they did a decade ago and it is reasonable to assume that they will look different ten years from now

- Companies that clearly understand their value proposition to clients benefit from focusing on it

- Good capital allocation is often the difference between good and great returns in the stock market

The information contained in this post is provided solely for informational and educational purposes and should not be construed as investment advice, a recommendation, or an offer to buy or sell any security. Nothing herein should be interpreted as an offer to sell or a solicitation of an offer to purchase any interest in any fund, vehicle, or strategy. Any such offering may only be made pursuant to formal offering documents and only to persons who are “accredited investors” as defined under Regulation D, Rule 501 of the Securities Act of 1933, in connection with a private offering conducted under Rule 506(b), and who also meet the requirements of Section 3(c)(1) of the Investment Company Act of 1940 or any other applicable exemption.

The views expressed represent the author’s opinions as of the date of publication and are subject to change without notice. The author has no obligation to update, amend, or supplement the information contained herein. Certain statements may constitute forward‑looking statements, which are inherently uncertain and involve risks, assumptions, and factors that could cause actual outcomes to differ materially.

Any references to past performance, investment examples, or specific securities are for illustrative purposes only and do not indicate or guarantee future results. The discussion of any strategy, concept, or thesis is not a recommendation or endorsement and should not be relied upon when making investment decisions. All investments involve risk, including the potential loss of principal.

Readers should conduct their own independent analysis and consult with their own financial, legal, tax, or other professional advisors before making any investment decision.