Will Thorndike vs. Mr Market

When good capital allocation is not enough...

Roughly half the books I read can be described as work-related. They would usually be either business biographies, such as Shoe Dog by Phil Knight, or investment process texts, such as Competition Demystified by Bruce Greenwald. Some books straddle both genres, with investment lessons drawn from the histories of the businesses analyzed. I think one of the better books from the latter category is The Outsiders by Will Thorndike.

The Outsiders argues that extraordinarily long-term shareholder returns are driven by exceptional capital allocation—how CEOs deploy cash through acquisitions, buybacks, dividends, debt, and reinvestment. By studying eight unconventional CEOs, The Outsiders shows that disciplined, rational capital allocation can create vastly more value than traditional management practices focused on growth, scale, or corporate prestige.

Given my focus on capital allocation, the central message of The Outsiders clearly resonates. Each of the cases presented in the book is a clear example where long-term returns have been enhanced through superior capital allocation. That said, a few years after I read the book, the part I remember is not the specific business story but a paragraph that was included almost in passing as a prediction (in 2012) near the end of the book:

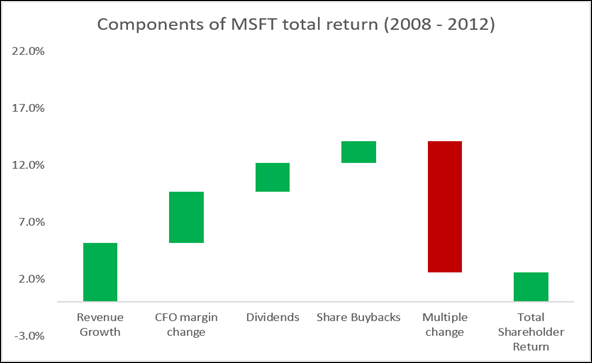

The interesting thing about this comment is that at least one of the companies mentioned has been doing for years exactly what Thorndike has been recommending in the book published in 2012. In the five years between 2007 and 2012, Microsoft generated roughly $115 billion in free cash flow, of which over $70 billion was returned to shareholders via one of those means. In the process, shares outstanding declined by roughly 12%. Most of the shares were bought at free cash flow yield between 9 and 11% - well above the yields paid by the high-quality bonds, which can serve as the opportunity cost benchmark for sound capital allocation. This is textbook good capital allocation.

The buybacks, despite their hypothetical value, failed to yield significant returns to shareholders, with Microsoft shares delivering just 2% per year returns during the five years. The 5% per annum revenue growth, buybacks, dividends, and margin expansion were almost fully offset by multiple contraction during that period. Rapturous market response this wasn’t.

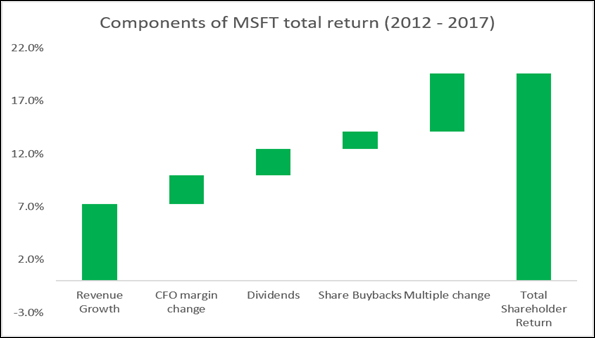

Now, if we contrast it with the performance in the next five-year period between 2012 and 2017, the picture is very different. While the fundamental factor contribution was identical at 14.1%, the total return was much more attractive at 19.6%. Multiple expansions added over 5% per annum, turning what would already be excellent shareholder returns into outstanding ones. So why the difference? It’s hard to attribute it to any one factor, but I think the following two matter:

First is the corporate management shift towards categories considered to be growing. In the five years in question, revenue growth accelerated from roughly 5% to 7%, an important data point but hardly sufficient to justify a major re-rating of the shares. However, in 2016, Satya Nadella, who had led the company since 2014, reorganized it into segments, taking the legacy Server & Tools segment and adding Azure cloud services, which were widely seen as a potential growth engine for the company.

The separation of the fast-growing division changed the rhetoric around Microsoft from a company milking its Windows and Office franchises to an entity that had potential for outsized growth. The market responded to the restructuring with an expansion in the P/E multiple. But another change was happening in the broader market.

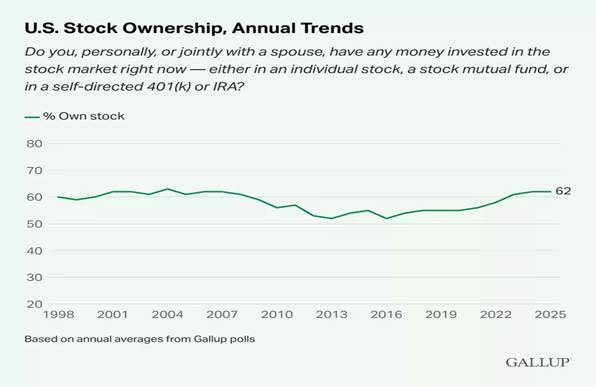

Before 2008, Microsoft consistently delivered revenue growth of 10%+ p.a. It was one of the most recognized companies in the world and was likely part of almost every retail investor’s portfolio. Before 2008, retail investors were increasing their allocation to the stock market and more likely than not were buying shares of Microsoft. The 2008 financial crisis triggered a long period of retail outflows from the stock market that lasted, not coincidentally, until the summer of 2013 – the period in which Microsoft experienced the multiple contraction.

Since 2013, the share of individuals with money invested in the stock market has stopped falling and, in 2016, started growing again. As a result, retail investors moved from net sellers to holders to eventually net purchasers of Microsoft shares.

This change in retail sentiment towards the stock market benefited not just Microsoft but other companies that managed to capture and retain retail investor attention. Together with Microsoft, companies like Apple, Amazon, Facebook/Meta, and, later, Nvidia have all been recipients of increasing retail stock market flows. This trend is one of the more likely explanations for why the largest companies are outperforming the rest of the market and experiencing multiple expansion relative to the other businesses.

The example of Microsoft shows that share performance is driven as much by what is happening to the marginal dollar entering the market as by fundamental factors. No amount of correct corporate decisions will lead to investors’ immediate delight if the money is flowing out of the stock market for one reason or another.

Sensitivity to market flows is not an excuse for poor corporate governance or capital allocation. On the contrary, I think fickle investor sentiment makes sound capital allocation even more important, since the company is less likely to be at the mercy of market conditions if it needs to raise capital or access bond financing. The sensitivity is, however, a reminder that finding the right companies is only half the battle. The other half is understanding the factors that lead to long-term performance and having the intestinal fortitude to withstand periods of adversity.

Disclaimer1

The information contained in this post is provided solely for informational and educational purposes and should not be construed as investment advice, a recommendation, or an offer to buy or sell any security. Nothing herein should be interpreted as an offer to sell or a solicitation of an offer to purchase any interest in any fund, vehicle, or strategy. Any such offering may only be made pursuant to formal offering documents and only to persons who are “accredited investors” as defined under Regulation D, Rule 501 of the Securities Act of 1933, in connection with a private offering conducted under Rule 506(b), and who also meet the requirements of Section 3(c)(1) of the Investment Company Act of 1940 or any other applicable exemption.

The views expressed represent the author’s opinions as of the date of publication and are subject to change without notice. The author has no obligation to update, amend, or supplement the information contained herein. Certain statements may constitute forward‑looking statements, which are inherently uncertain and involve risks, assumptions, and factors that could cause actual outcomes to differ materially.

Any references to past performance, investment examples, or specific securities are for illustrative purposes only and do not indicate or guarantee future results. The discussion of any strategy, concept, or thesis is not a recommendation or endorsement and should not be relied upon when making investment decisions. I, Firebird, and accounts managed or advised by Firebird may hold positions in companies mentioned here. All investments involve risk, including the potential loss of principal.

Readers should conduct their own independent analysis and consult with their own financial, legal, tax, or other professional advisors before making any investment decision