When the underdog wins

Lessons from Etsy's battle with Amazon Handmade

The fundamental investment process is naturally backward-looking, since it often begins with an analysis of historical financial statements. The main problem with relying on financial statements is that past performance may no longer be relevant. If the reason for extraordinary profits no longer exists (e.g., patent expiration) or if the business was disrupted by innovation or competition, then the last year’s numbers have little bearing on what the company will earn in the future.

With patents, it is very clear that the historical reason for the generation of excess returns no longer exists. As soon as it becomes legally permissible, competition swoops in and offers the same product at a lower price, which forces the former patent holder to lower its prices and profits. With other types of disruption, the catalyst for lower profitability is much less obvious and sudden. Competitive dynamics develop over time and can swing back and forth before ultimate outcome is obvious. Often enough the incumbents fight off the challengers and emerge with even stronger business fundamentals. Figuring out whether the business model can survive the challenge is one of the more interesting and rewarding exercises for the fundamental investors.

There is a category of investments that can be described as: “Company X is toast because Company Y will make their business uneconomic!” Given its status as the “Everything Store,” on more than one occasion, the company Y is Amazon.com. Jeff Bezos, founder of Amazon, is famous for coining the phrase “your margin is my opportunity,” and he means it.

The list of companies that fell victim to Amazon over the years is long. Borders, Toys R’ Us, Circuit City… None of them managed to adapt their business models to the online competition and eventually went bankrupt. Given the track record, when a headline comes out that Amazon is expanding into a new industry, the market takes notice, and valuations of existing players in that industry suffer.

That said, Amazon’s track record is not perfect. Over the years, it has attempted to expand into several industries where the effort ultimately proved futile. Does anyone remember Amazon Destinations (travel website), Amazon Restaurants, and Amazon Local? I don’t think so.

Given the wide range of outcomes, I’ve realized that the best way to assess whether a company is likely to be disrupted by Amazon (or anyone) is to apply the “10x better” framework. The idea is as follows: Is the challenger’s product 10x better than the existing solution because it delivers better results, is cheaper, more convenient, or some combination of the above?

Compared to brick-and-mortar retailers, Amazon offered more choice, better prices, and the convenience of shopping in your underwear. This was 10x better than going to a physical store, which is why old-line retailers trying to hold on to their historical profits failed to compete effectively.

On the other hand, compared to Booking.com or Expedia, Amazon’s travel website offered, at best, a product similar to what was already on the market and could not offer better prices, since hotel owners are often prohibited from price discrimination under the terms imposed by the OTAs. Amazon could not come up with a 10x better offer, which is why Booking.com and Expedia effectively fought off challenges from Amazon, Google, and other contenders that have come along up to this point.

Another example of a company challenged by Amazon is Etsy.com, an online marketplace for handmade goods. Etsy was listed in April 2015, and just six months later, Amazon launched Amazon Handmade – a marketplace for handmade goods. Etsy stock, already struggling with decelerating growth, took another leg lower, with the market understandably concerned about the viability of its business given the presence of such a large competitor.

To apply the 10x better framework to any business, it is important to understand who the real customers are. In the case of Etsy, it wasn’t the shoppers but the artisans producing the goods. These artisans had the option to (and often did) sell their goods on both Amazon and Etsy (and their own websites), and the question was which venue provided them with the easiest way to market their goods and would gain relative share.

This is where Etsy excelled. It worked on artisan engagement and added features such as a manufacturing assistance program (helping artisans find spare manufacturing capacity at other small-scale manufacturers), direct billing, and PayPal integration. For Amazon, a company with hundreds of billions in sales, going into the business of matching a curtain designer with a curtain manufacturer did not make sense – for Etsy, it did.

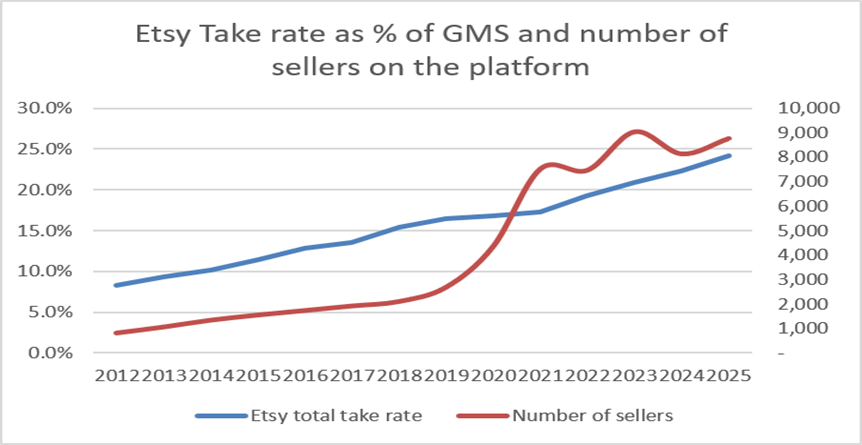

These services didn’t just increase seller captivity; they also generated significant revenue for Etsy, enabling the company to capture a higher share of each sale. In 2016, merchants paid roughly 9.5% of the sale price to Etsy for access to the marketplace and payment processing, and another 3.1% for additional services the company offered. The artisans were happy to pay the fees since it allowed them to focus on the part of the process they enjoyed the most – the creative one – while Etsy took care of all the boring bits.

By understanding the artisans better than Amazon did, Etsy became the 10x better option. Moreover, by making it easy to create, Etsy offered more people the opportunity to pursue their passion, thereby expanding the addressable market.

Between 2015 and 2023 Etsy grew the number of sellers at an average of 25% per year. Over the same period, revenues and operating cash flow grew at even faster rates of 33% and 60%, respectively. The stock price, thanks in large part to the COVID boom, went from below $10 in 2015 to over $200 in 2021. In 2023, even after the positive impact of the pandemic had faded for ETSY, its shares still traded above $80, providing a significant return for anyone who bet on the underdog against a much larger competitor.

Today, Etsy shares are trading at around $70, indicating flat or negative returns over the last couple of years. The reason for this is a lesson in itself. Etsy, especially after COVID, to maintain the growth rates, continued to take a larger share of the seller’s top-line revenues. At some point, the fees the company charges become too high, which starts to destroy the economics for its customers, which resulted in artisans leaving the ecosystem.

In 2023, Etsy’s total take rate exceeded 20%, coinciding with the platform’s peak in seller count. Since then, the take rate has continued to grow, but revenue growth has slowed dramatically. Ironically enough, if there ever were a chance for someone to challenge Etsy as the go-to marketplace for handmade goods, the time would be now when artisans are seemingly incentivized to look for alternatives, rather than when the company was young and hungry to win.1

The information contained in this post is provided solely for informational and educational purposes and should not be construed as investment advice, a recommendation, or an offer to buy or sell any security. Nothing herein should be interpreted as an offer to sell or a solicitation of an offer to purchase any interest in any fund, vehicle, or strategy. Any such offering may only be made pursuant to formal offering documents and only to persons who are “accredited investors” as defined under Regulation D, Rule 501 of the Securities Act of 1933, in connection with a private offering conducted under Rule 506(b), and who also meet the requirements of Section 3(c)(1) of the Investment Company Act of 1940 or any other applicable exemption.

The views expressed represent the author’s opinions as of the date of publication and are subject to change without notice. The author has no obligation to update, amend, or supplement the information contained herein. Certain statements may constitute forward‑looking statements, which are inherently uncertain and involve risks, assumptions, and factors that could cause actual outcomes to differ materially.

Any references to past performance, investment examples, or specific securities are for illustrative purposes only and do not indicate or guarantee future results. The discussion of any strategy, concept, or thesis is not a recommendation or endorsement and should not be relied upon when making investment decisions. I, Firebird, and accounts managed or advised by Firebird may hold positions in companies mentioned here. All investments involve risk, including the potential loss of principal.

Readers should conduct their own independent analysis and consult with their own financial, legal, tax, or other professional advisors before making any investment decision