What I learned from following a legend.

Several people are undisputedly among the pantheon of Value Investing Legends. Warren Buffett, Charlie Munger, and Benjamin Graham are the names that come to mind first, but a credible case can be made for a few others, including the subject of this post, John Malone.

John Malone’s story starts with Tele-Communications Inc. (TCI), which he ran from 1973 to 1998. This company, through a series of acquisitions, became the largest US Cable operator before being sold to AT&T for $32 billion in equity value, delivering 900x to the original investors. In addition to the money paid by AT&T, Malone’s investors over the years received several assets in spin-off transactions, including Liberty Media, Discovery Communications, QVC, Liberty Interactive, Liberty Broadband, and Liberty Global, all of which have gone on to deliver strong returns to investors in part due to additional spin-offs. In total, there were 40 or so different companies, of which twelve are public today, that can trace their roots to the original TCI.

Most of the companies that Malone invested in can be broadly defined as media companies. It’s a large tent that includes infrastructure (cable companies), traditional content (Discovery, Starz), online properties (Tripadvisor, Expedia), or some combination of the above (Sirius XM). The feature they share is that the companies can hold significant leverage due to their predictable cash flows. Malone often used debt to acquire additional assets, which were in turn leveraged to fund further acquisitions.

Given the reliance on debt funding, one of the keys to Malone’s success was that most of his career took place in a declining interest-rate environment. While he was in charge of TCI since 1973, the acquisition machine didn’t really get going until the 1980s when interest rates started falling, and additional funding sources became available, including the junk bonds popularized by Michael Milken.

To be clear, declining interest rates are not the only reason Malone achieved the success that he had. He proved to be a superior operator, willing to buy distressed assets when their future was far from certain. He also managed his companies religiously to generate as much cash as possible, in part by minimizing taxes so he could reinvest the money.1

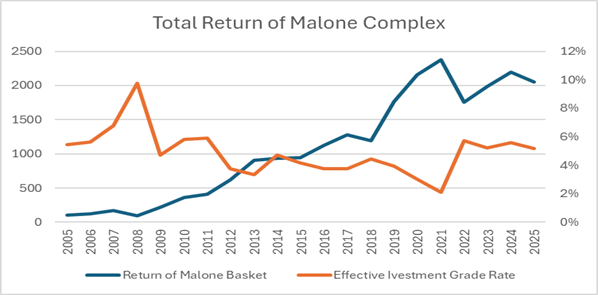

The above factors were important for the success, but one data point suggests that none were as important as the interest rates. Looking at the performance of the Malone Index2 over the last twenty years, it seems that his returns stayed strong until 2020 but have stagnated since then, as borrowing rates rose after the Covid bottom. Moreover, there is a clear negative correlation: the Malone index underperformed in 2007 and 2018 – periods when interest rates were rising.

My takeaway from the above is as follows: even the best investors have difficulty delivering returns when they face macroeconomic headwinds that threaten the key elements of their strategy.

The second thing to consider is which companies were responsible for most of the value growth and why. Looking at the performance of various businesses over the last decade, the ones that have done best were those with steady or growing underlying demand and pricing power – Live Nation and Formula One. The ones that struggled are those being disrupted by new technologies that give their customers alternatives. Home Shopping Network operator Qurate Retail is having trouble staying relevant as smartphones provide endless entertainment and personalized shopping recommendations. SiriusXM’s paid subscription service is more expensive than Spotify, and you don’t get to choose your own music. Technological disruption combined with leverage rarely leads to good investment outcomes. At a risk of being accused of heresy, it is possible that John Malone, for all his prowess in buying and running companies, may not be as good at selling them when he should have.

As far as my involvement with Malone companies – it’s fair to say that I’ve dabbled… The investments included Tripadvisor from 2015 to 2018, SiriusXM from 2016 to 2019, and Discovery Communications from 2015 to 2022. Each one is an interesting example that shows both the benefits and the limitations of following anyone religiously, independent of how good their track record is.

With Tripadvisor, I was attracted by its status as the default source for anyone planning a vacation, strong relationship with hotels, and an emerging experiences business that was viewed as a liability, but I felt was a major potential source of value for the company. The operational thesis largely played out as expected, with the company’s EBITDA profitability improving by roughly 30% over the three years, but that did not lead to an improvement in valuation due to multiple contraction. I sold for various reasons, one of which was management’s comments that denigrated user-generated content, which I felt was the main feature that distinguished the company from many competitors. If the CEO didn’t appreciate all that content, why should I?

“If I’m going to London, the last thing I want to do is read 1,000 hotel reviews. I want inspiration.”

– Steven Kaufer, CEO of Tripadvisor, in a 2018 interview.

Sirius XM, by the time I invested in it, was the undisputed monopolist in satellite radio. The company was formed with Malone’s help by combining two companies – Sirius and XM Radio, which, before the combination, had competed to the brink of mutual insolvency. Once combined, the business became a cash-flow-generating machine, in part thanks to being automatically pre-installed in 75% of vehicles sold in the US, which significantly reduced their customer acquisition cost.

The company was using all the cash it generated to buy back shares, which effectively increased Malone’s controlling stake, since his company, Liberty Sirius, was not selling into the buybacks. The buybacks were a smart form of capital allocation because shares were trading at a higher yield than the company paid on its debt. As a shareholder, I appreciated both the value generated by the buybacks and the fact that they served as a natural source of demand for the company’s shares, thereby reducing potential downside.

Thanks to rising earnings driven by price increases and buybacks, Sirius XM shares delivered low double-digit returns between 2016 and 2019, but I felt there were signs of trouble on the horizon. The valuation the market was willing to pay for car manufacturers’ shares was coming down, which, to me, served as a clear sign of potential distress for Sirius XM, since new car sales were a key source of new subscribers for Sirius XM.

The story of Discovery Communications probably deserves its own post. For now, it is sufficient to say that i bought it when i thought the merger with Scripps network would bring significant benefits of scale due to similar content, and sold it when I thought that the merger with Warner Brothers brought significant risks precisely because the content of the two companies was very different.

The one thing in common for all three of my ventures into the Malone universe is that the companies were trading at attractive valuations at the time of the investment. These investments led to solid returns but nothing like the 30%+ IRRs that Malone generated for his investors in the 80s.

Counterintuitively, the attractive valuation could be the reason why outsized returns were not available. Malone’s track record is well known, and companies were optically cheap. This means that the market was pricing in the emerging disruption threats on the horizon and the limitations of Malone’s model in dealing with them.

There is an old joke that when someone is looking for something good, cheap, and fast, they must pick just two out of three. Investing equivalent is quality, value, and growth. More often than not, only two of the three attributes are available at any given time, and we, as investors, have to understand the trade-offs and their implications.3

Takeaways:

- Most exceptional investment returns are generated in a macro environment that is uniquely beneficial to a particular strategy. Different macro environment – different outcomes

- There is usually a good reason for why something is trading at a cheap price, especially when the company is run by a person known for superior investment returns.

John Malone’s story is best told in the 2002 book Cable Cowboy by Mark Robichaux.

Companies included are Atlanta Braves, Charter Communications, Discovery Communications, Formula One, Liberty Latin America, Liberty Media, Live Nation, Qurate Retail, Sirius XM, Starz, Tripadvisor. I did not include tracking stocks on some of the underlying assets since their performance would be similar. The annual performance of each company is market cap weighted in order to calculate the Malone Performance Index

The information contained in this post is provided solely for informational and educational purposes and should not be construed as investment advice, a recommendation, or an offer to buy or sell any security. Nothing herein should be interpreted as an offer to sell or a solicitation of an offer to purchase any interest in any fund, vehicle, or strategy. Any such offering may only be made pursuant to formal offering documents and only to persons who are “accredited investors” as defined under Regulation D, Rule 501 of the Securities Act of 1933, in connection with a private offering conducted under Rule 506(b), and who also meet the requirements of Section 3(c)(1) of the Investment Company Act of 1940 or any other applicable exemption.

The views expressed represent the author’s opinions as of the date of publication and are subject to change without notice. The author has no obligation to update, amend, or supplement the information contained herein. Certain statements may constitute forward‑looking statements, which are inherently uncertain and involve risks, assumptions, and factors that could cause actual outcomes to differ materially.

Any references to past performance, investment examples, or specific securities are for illustrative purposes only and do not indicate or guarantee future results. The discussion of any strategy, concept, or thesis is not a recommendation or endorsement and should not be relied upon when making investment decisions. All investments involve risk, including the potential loss of principal.

Readers should conduct their own independent analysis and consult with their own financial, legal, tax, or other professional advisors before making any investment decision.