The Chipotle Lesson

When being right still turned out to be wrong.

The average holding period for U.S. stocks has collapsed from roughly 7-8 years in the 1950-1960s to less than one year in the 2020s1. For a long-term investor, this fact should be both scary and exciting. The majority of the market operates on different timelines, and how one deals with it depends on the person’s comfort with looking foolish from time to time.

One example that comes to mind is Chipotle (CMG). The company started in 1993 from a single store near the University of Denver and created the “fast-casual” concept that spread across the country. By 2015, the company was operating over 2,000 stores, which were generating over $2m in sales per store and delivering 70%+ cash-on-cash annual returns on the opening costs. The market was putting a well-deserved premium on the company, with the shares trading at 50x earnings.

In August 2015, the norovirus outbreak linked to a Chipotle store in Simi Valley, CA, sickened over 200 customers and put a blemish on what had been, before this, a success story. Same-store sales growth fell from 10%+ in 2014 but remained positive, indicating that most customers were comfortable with a small side of risk accompanying their burrito. The Simi Valley incident was followed by a salmonella outbreak in Minnesota in August and an e. coli scare in Washington and Oregon in October. The second norovirus outbreak in Boston sickened another 150 customers. The continuous stream of bad news changed the risk calculation from the diners’ point of view, leading to double-digit declines in visits to shops.

While the market largely ignored the first norovirus incident, it definitely noticed the subsequent events. Chipotle’s shares fell by almost 50% between September 2015 and January 2016. Aside from obvious concerns for the health of the diners, one of the biggest questions being asked was whether Chipotle’s “food with integrity” concept, which relies on fresh ingredients cooked on site, could even be scaled to thousands of restaurants without triggering a stream of one-off incidents as the ones that plagued the company in the second half of 2015. For anyone considering investing in the company, the key question was whether the consumers will ever feel that a trip to Chipotle does not come with a slight risk of food poisoning.

The analysis of past incidents2 suggested that consumers’ affinity for their favorite type of fast food usually proves more enduring than the memory of past safety issues. The same turned out to be the case for Chipotle…or so it seemed.

By the second quarter of 2017, sales per store were recovering, and the company looked to be gaining back customer’s trust, when yet another norovirus outbreak, this time in Virginia, hit the company’s results. If you, as I did, invested in the company under the assumption that food safety issues are behind Chipotle, in July 2017 you looked rather silly. Being contrarian is only fun if you are proven right, and at the time, that looked like an increasingly unlikely outcome.

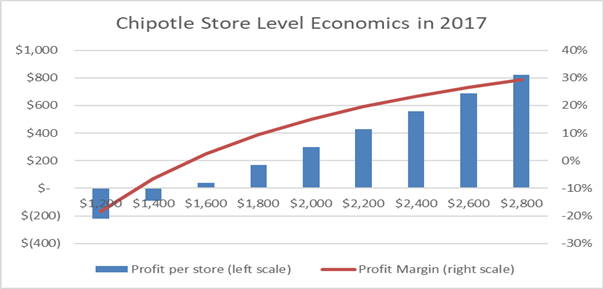

Thankfully, in addition to the review of past food safety incidents, the analysis of Chipotle’s business model and balance sheet suggested that it can survive even the latest calamity. The key to understanding it was to look at store-level economics and split costs into fixed and variable.

Labor, rent, utilities, and other similar costs were pretty much fixed and totaled roughly $1 million per store per annum. Food costs were variable and usually around 35% of sales. Putting the two together helped quantify the uncertainty and define the bet as follows: “Does one think that Chipotle sales per store are higher or lower than X?”

In 2016, with food safety concerns at their peak, Chipotle still delivered over $1.8 million per store, putting the company comfortably in the black and generating high enough returns to justify chain expansion. If sales per store return to $2.4 million (2014 levels), then profitability per store triples. An investor could construct a probability tree of possible outcomes and derive a weighted estimate of Chipotle’s earnings. Probabilistic thinking is one of the few advantages a long-term investor has in a market that seems to operate in short-term absolutes.

The curious thing about the calculations above is that even though the sell-side analysts were comfortable projecting a recovery in Chipotle’s sales, they were not considering the cost structure of the stores. Most reports I saw at the time kept margins at about the same level as the company delivered in 2017, when sales were still low.

One person who did make a personal bet on the company’s cost structure is Brian Niccol, formerly the head of the Taco Bell division of Yum Brands, who was brought in to “professionalize” Chipotle’s operations. Before agreeing to take the role, Mr. Niccol negotiated a pay package with specific awards for achieving restaurant-level cash flow margins set at levels that looked ambitious compared to recent results but were rather pedestrian when evaluated against pre-2015 levels.

Whether through skill or through good timing, Mr. Niccol delivered. In 2018, same-store sales grew to around $2m per store, triggering a recovery in margins, a new CEO’s pay package, and a 70% increase in the company’s valuation. This would seem like the time to declare a success for contrarianism, but unfortunately, this is exactly when my tendency to swim against the tide led me to a decision that would prove much costlier – selling too early.

Instead of celebrating that the company was finally doing well, I remembered that dreadful feeling of fearing the breaking news of yet another norovirus outbreak that could have ruined Chipotle’s reputation with diners for good. The flip side of looking for reasons to buy the companies that market hates is looking for reasons to sell the companies that market likes. In this case, Mr. Niccol’s decision to move Chipotle’s headquarters from Denver to his home in California looked like exactly the type of action that the CEO who cares about delivering the best returns to shareholders should not be doing. Following the announcement of headquarters move, I decided that the risk/reward was no longer in my favor and sold the stock.

Instead of looking for reasons to sell, the right thing to do would have been to focus on the company’s actions and consider the potential impact of management’s initiatives on store sales using the same probabilistic thinking that allowed me to invest in the company in the first place.

The key thing to consider should have been not the headquarter locations, but the Chipotle’s initiative to roll out second production lines in stores to service takeout and delivery orders. Anyone who spent time in Chipotle’s lunch rush line realized that the company’s problem was not demand but throughput. The second line allowed the capture of incremental orders and improved sales per store, while increasing fixed costs only slightly. The net effect of installing the second line was growth in revenue per store to over $2.6 million and a more than doubling of Chipotle’s free cash flow generation. The share price followed the results, with more than a 6x increase from the level at which I sold to the eventual peak in 2024, when same-store sales seemingly stabilized at a new, higher level.

The lesson from this situation proved expensive but valuable. It is always important to consider the levers the company controls – such as operational improvements and growth initiatives and their impact on results. It is just as likely that the market is underpricing them when the shares are doing well as when the shares are doing poorly.

Takeaways:

- Probabilistic thinking helps with analyzing situations with wide range of outcomes

- When company finally starts doing well consider both the likelihood of results improving even further as well as the downside

Disclaimer3

https://www.visualcapitalist.com/the-decline-of-long-term-investing/

Yum Brands got embroiled in a scandal in China related to the KFC brand and sourcing practices. While the issue there was contained to just China and did not jeopardize the whole global operations, the problems did impact the sales in the country which prior to that was a major source of growth for Yum Brands. Consumer stayed away for a little while but eventually came back to the brands once the company publicly addressed the supply chain problems.

In another case, more like Chipotle’s, Wendy’s restaurants were the source of an e. coli outbreak in 2005 that led to illnesses and hospitalizations. Once again, the consumers stayed away and the stock reacted negatively for a bit but ultimately both came back.

The information contained in this post is provided solely for informational and educational purposes and should not be construed as investment advice, a recommendation, or an offer to buy or sell any security. Nothing herein should be interpreted as an offer to sell or a solicitation of an offer to purchase any interest in any fund, vehicle, or strategy. Any such offering may only be made pursuant to formal offering documents and only to persons who are “accredited investors” as defined under Regulation D, Rule 501 of the Securities Act of 1933, in connection with a private offering conducted under Rule 506(b), and who also meet the requirements of Section 3(c)(1) of the Investment Company Act of 1940 or any other applicable exemption.

The views expressed represent the author’s opinions as of the date of publication and are subject to change without notice. The author has no obligation to update, amend, or supplement the information contained herein. Certain statements may constitute forward‑looking statements, which are inherently uncertain and involve risks, assumptions, and factors that could cause actual outcomes to differ materially.

Any references to past performance, investment examples, or specific securities are for illustrative purposes only and do not indicate or guarantee future results. The discussion of any strategy, concept, or thesis is not a recommendation or endorsement and should not be relied upon when making investment decisions. I, Firebird, and accounts managed or advised by Firebird may hold positions in companies mentioned here. All investments involve risk, including the potential loss of principal.

Readers should conduct their own independent analysis and consult with their own financial, legal, tax, or other professional advisors before making any investment decision

Your sell decision used a different framework than your buy decision. Thats the actual lesson. You built a probabilistic model for the downside and then abandoned it for a narrative when the upside arrived.

Most mistakes in investing arent in the analysis, there in the inconsistency of how it gets applied depending on which direction the position is moving.