Molecules Matter!

Coming into the year, it seemed that the only things that mattered for the global economy were the pace at which new data centers could be built and the impact of artificial intelligence on employment and productivity. The war in Iran and the subsequent disruption to global energy supplies served as a reminder that, while we may be transitioning to the world of electrons, our daily lives are still dominated by molecules.

For the better part of the last hundred years, this molecular world has been dependent on oil and gas. The hydrocarbons are extracted from the ground and used to power, heat, light, and outfit almost every aspect of our daily lives. Thanks to the rising living standards of a growing population, the demand for hydrocarbons is steadily increasing, even as alternatives are emerging that could replace/augment some current use cases.

Given the described dynamic and the importance of oil and gas to daily life, it is a wonder that the world has come to rely on an equilibrium in which spare production capacity is less than 3% of demand and hydrocarbon supply is delivered via long and complicated logistics chains. The war in the Middle East and the subsequent closure of the Strait of Hormuz, through which almost 20% of global oil production is transported, served as an unwelcome reminder of how fragile the equilibrium truly is.

The ultimate resolution of this conflict is still in question, but we think that, regardless of when and how quickly deliveries from the Gulf regions are restored, the world is unlikely to remain comfortable with the minimal spare capacity in hydrocarbon production and with reliance on any single region.

In a similar setting, the global economy was first shocked by the Arab oil embargo (1973-74) and then by the Iranian revolution in 1979, with each incident impacting roughly 7% of global oil production. Like today, before the disruptions, the supply and demand were evenly matched. What followed these events was a major investment period that more than doubled the amount of capital committed to finding new sources of hydrocarbons. As a result, several new sources of energy, such as the Gulf of Mexico, the North Sea, and Cantarell field in Mexico, were discovered.

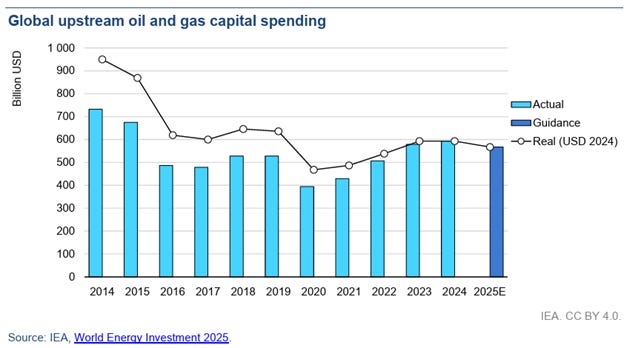

Coming back to today, before the Iran war, oil and gas investments were at a low. Since 2014, volatility in oil prices and concerns about the sustainability of demand amid the push for renewable energy have led to a decline in interest in developing new projects. While investment has recovered a bit in recent years due to long-term oil prices stabilizing above $60, the total remains roughly 40% below 2014 levels in nominal terms.

The disruptions to shipping through the Strait of Hormuz affect roughly 20 million barrels of daily production. The current ceasefire raises hope that the problems will prove temporary, but oil-importing countries are becoming acutely aware of the danger of being overly dependent on any single hydrocarbon source, no matter how stable it may seem at the time. We think that, just as in the 1970s, the response will be to seek alternatives. There is some debate over whether they will come in the form of additional oil and gas sources or increased penetration of renewables, but the most likely scenario is that it will be both, and that investments in hydrocarbons will be well above 2014 peaks.

Disclaimer1

The information contained in this post is provided solely for informational and educational purposes and should not be construed as investment advice, a recommendation, or an offer to buy or sell any security. Nothing herein should be interpreted as an offer to sell or a solicitation of an offer to purchase any interest in any fund, vehicle, or strategy. Any such offering may only be made pursuant to formal offering documents and only to persons who are “accredited investors” as defined under Regulation D, Rule 501 of the Securities Act of 1933, in connection with a private offering conducted under Rule 506(b), and who also meet the requirements of Section 3(c)(1) of the Investment Company Act of 1940 or any other applicable exemption.

The views expressed represent the author’s opinions as of the date of publication and are subject to change without notice. The author has no obligation to update, amend, or supplement the information contained herein. Certain statements may constitute forward‑looking statements, which are inherently uncertain and involve risks, assumptions, and factors that could cause actual outcomes to differ materially.

Any references to past performance, investment examples, or specific securities are for illustrative purposes only and do not indicate or guarantee future results. The discussion of any strategy, concept, or thesis is not a recommendation or endorsement and should not be relied upon when making investment decisions. All investments involve risk, including the potential loss of principal.

Readers should conduct their own independent analysis and consult with their own financial, legal, tax, or other professional advisors before making any investment decision.